Paying off your mortgage early can be freeing. Who wouldn’t love owning a home free and clear? But did you know that paying your loan early isn’t only for the wealthy? Anyone can do it with small, consistent steps.

But paying off a house early isn’t for everyone; there are pros and cons to consider. So here’s what you should know about when deciding should a mortgage be paid off early.

Paying off your Mortgage Early – An Overview

At the mortgage closing, you signed documents stating you would make your principal and interest payments on time. But what if you want to pay extra?

Most lenders allow you to pay your mortgage early; prepayment penalties aren’t as prevalent today. But you’re likely talking about hundreds of thousands of dollars, so it won’t happen overnight or even in a couple of years.

You can pay your mortgage off early with small, consistent, extra payments or apply any lump sum funds you receive throughout the mortgage term.

What can you Save by Paying off a Mortgage Early?

Each borrower will see different savings paying a mortgage off early. How much you save depends on how early you pay the balance down and when you pay it. Payments made earlier in the term will save you more money because you decrease the amount you pay interest monthly.

For example, if you have a $100,000 mortgage at 5% on a 30-year fixed loan, your principal and interest payment is $536.82, and you’d pay $93,255.78 in interest over the 30 years.

If you pay an extra $100 a month, you’d pay the loan off in 31 years and four months and pay only $62,676 in interest. That’s a savings of $30,580.

You'd save even more if you paid more than $100 a month or made lump sum payments greater than $1,200 a year.

How to Pay off a Mortgage Early

There are several options to pay a mortgage off early. The right way for you is the one you can afford the most.

Extra Monthly Payments

If you have leeway in your budget, consider increasing your monthly payments. As our example showed, even an extra $100, a month can shorten your loan term and save you thousands in interest.

Bi-weekly Payments

Rather than making monthly payments, consider bi-weekly payments. This method doesn’t require you to pay more each month. Instead, you split your mortgage payment in half and pay that amount every two weeks. Because there are 52 weeks a year, you make 13 full monthly payments or one extra mortgage payment per year.

Use Windfalls to Pay Down your Mortgage

If you have windfalls, such as a tax refund, consider using them to pay the mortgage annually. If you need a benchmark, aim to make one extra mortgage payment annually. Of course, if you can pay more, it will pay your mortgage down faster.

Refinance to a Shorter Term

If you can afford a higher monthly payment, consider refinancing to a shorter term. For example, 15-year loans have lower interest rates than 30-year loans typically. The lower interest rate and higher principal payment will help you own your home faster and save thousands of dollars in interest.

Make 15-Year Payments on a 30-Year Term

If you’re uncomfortable with refinancing and committing to the higher payment, use a mortgage calculator to determine the 15-year payment. Then, you can make those payments, applying them to the principal balance without requiring it. The money counts as extra principal and will pay your loan down faster, putting you on track to pay your loan off in 15 years.

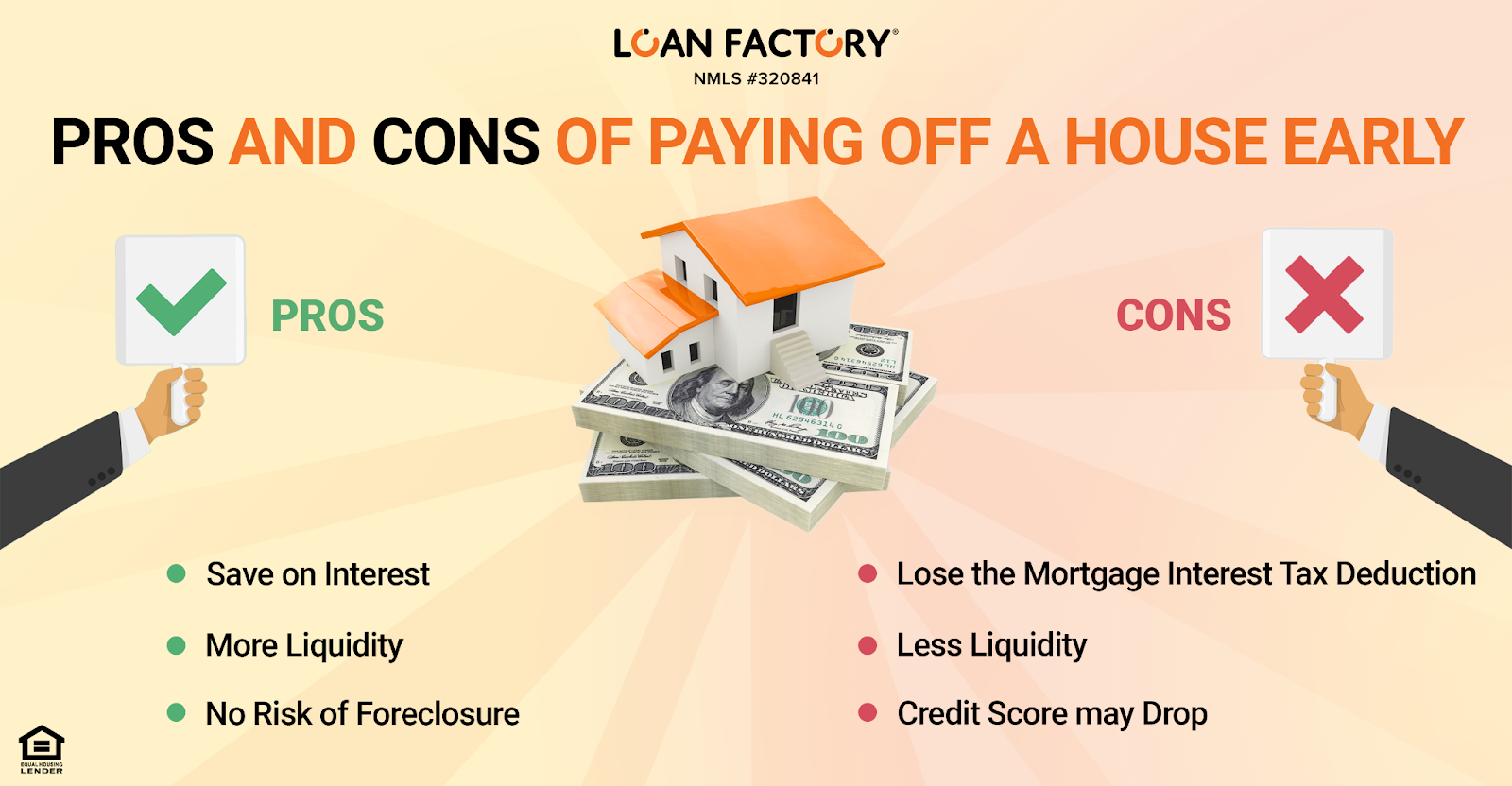

Pros and Cons of Paying off a House Early

Like any financial decision, paying off a house early has pros and cons. Here’s what to consider.

Pros:

Save on Interest

You’ll pay less interest when you pay a house off early. Even if you don’t make 15-year payments and only pay an extra $50 - $100 monthly, it lowers your principal balance and the interest owed. So you’ll see savings no matter how much extra you pay.

More Liquidity

You won’t have to worry about tying up your income in monthly mortgage payments. Instead, when you pay the house off early, you free up your budget, giving you more room to save an emergency fund or invest in your future.

No Risk of Foreclosure

Paying off your mortgage early eliminates the risk of foreclosure. Since you own the home outright, the bank can’t take it from you. Of course, you must still keep up with the real estate taxes and home insurance, but the foreclosure risk ends with a paid-off mortgage.

Cons:

Lose the Mortgage Interest Tax Deduction

If you itemize your tax deductions, you’ll lose the mortgage interest tax deduction when you pay your mortgage off early. Even as you pay your mortgage down faster, you’ll pay less interest, reducing the tax write-off.

Less Liquidity

Tying your money up in your house isn’t very liquid. If you have a financial emergency, you can’t sell your house instantly and get the money back. While you can do a cash-out refinance or sell your home, it can take several months.

Credit Score may Drop

Your credit score combines credit mixes, payment history, and credit utilization. So, for example, if you pay your mortgage off early, you lose one type of credit and a timely payment history. The damage to your credit score may not be huge, but it’s something to consider.

Final Thoughts

Paying your mortgage early is a great goal, but it’s not for everyone. But, even if you make a small extra monthly payment, it can save you thousands of dollars.

There are many ways to pay your mortgage off early that don’t have to break the budget. Instead, consider making an effort to make even a small extra payment each month, and you’ll see the savings at the end of the term.